The regulatory landscape for consumer finance is shifting faster than ever, with the Federal Reserve Board, Consumer Financial Protection Bureau (CFPB), and state agencies tightening compliance expectations across the board. In February 2026, a wave of amendments rolled out—most notably in Regulation B (ECOA) and Regulation V (FCRA)—mandating new contact information and summary disclosures that could ripple through credit unions, fintech lenders, and online marketplaces. Below is a deep dive into how these changes impact institutions today, what they mean for borrowers, and the strategic steps you can take to stay ahead.

Regulation B Updates: The New Contact-Info Mandate

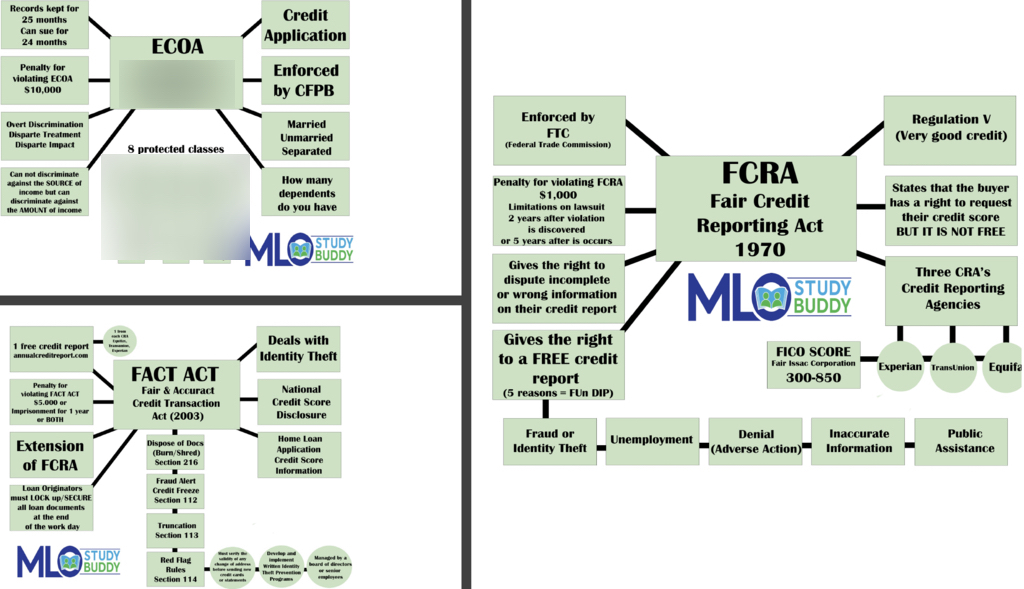

Regulation B’s latest revision requires every adverse‑action notice to list updated contact details for a range of federal agencies—CFPB, OCC, FDIC, NCUA, FTC, and others. This seemingly minor tweak has far‑reaching implications: lenders must re‑engineer their notification templates, update automated email systems, and ensure that legal teams review every template for compliance.

For fintech platforms that generate thousands of notifications daily, the change means a quick audit of all back‑end scripts. The CFPB’s own guidance, published in March 2026, clarifies that the new contact information must appear in the same location as the original notice, not appended at the bottom. Failure to comply could lead to enforcement actions or loss of customer trust.

- Key Takeaway: Revise all adverse‑action templates by March 20, 2026.

- Risk: Non‑compliance may trigger CFPB investigations and civil penalties up to $10,000 per violation.

Credit unions that rely on third‑party service providers must coordinate with those vendors to propagate the changes across all customer-facing channels. The ripple effect can also touch marketing materials, FAQ pages, and even mobile app notifications.

Regulation V: Summary of Consumer Rights Gets a Facelift

Under Regulation V, consumer reporting agencies are required to provide a “Summary of Consumer Rights” whenever they disclose credit information or issue a score. The 2026 amendments correct the contact details for the OCC, FDIC, and NCUA within the summary form. While the format remains unchanged, the updated contact list ensures that consumers can reach the appropriate agency quickly if they suspect inaccuracies.

These changes are especially pertinent for online lenders that pull credit reports via APIs. Each API call must now include a properly formatted summary in the response payload. Failure to do so could expose lenders to consumer lawsuits and regulatory scrutiny.

| Agency | Contact Type |

|---|---|

| OCC | Consumer Complaint Hotline |

| FDIC | Customer Service Email |

| NCUA | Phone Support Line |

Fintechs that partner with credit bureaus should verify that the summary form they receive aligns with the CFPB’s latest specifications. The CFPB has provided a comprehensive checklist to help firms audit their processes.

Regulation Z: TILA Compliance Amidst New Contact Corrections

TILA, as codified in Regulation Z, remains the backbone of consumer credit disclosures. The recent amendments correct contact information across appendices A, B, and C—pertaining to state requests for consistency determinations, exemption applications, and official interpretation requests.

For mortgage servicers and auto lenders, this means updating every disclosure document—from loan estimates to periodic statements—to reflect the new contact details. Lenders that outsource these documents risk non‑compliance if they rely on outdated templates.

- What’s New: Updated CFPB, OCC, and NCUA contact information in all consumer disclosures.

- Why It Matters: TILA violations can trigger class actions and hefty fines.

The CFPB has issued a detailed guidance document outlining the precise changes. Lenders should review it closely to avoid inadvertent breaches.

Interstate Land Sales: Regulation J’s Contact Corrections

The most recent amendments to Regulation J affect land developers who must provide prospective buyers with model forms and clauses—now updated with new CFPB contact details. While the primary focus of the amendment is contact accuracy, it underscores a broader trend: regulators are tightening the chain of accountability across every consumer-facing document.

Real estate platforms that offer financing options or escrow services need to audit their contract templates for compliance. The March 20, 2026 compliance date applies universally—no grandfathering for older contracts.

Fintechs’ Strategic Response: Building a Resilient Compliance Program

With the CFPB’s “resilience” stance—maintaining core statutes while selectively relaxing enforcement—the onus is on firms to keep their compliance engines humming. Here are three actionable steps:

- Automate Template Updates: Deploy a central document management system that pushes updates to all templates when new regulatory changes occur.

- Continuous Monitoring: Implement real‑time monitoring of consumer complaints and audit logs to catch potential violations before they snowball.

- Stakeholder Education: Conduct quarterly training for sales, marketing, and legal teams on the latest regulatory shifts.

By embedding compliance into the product lifecycle rather than treating it as a post‑hoc check, fintechs can reduce risk while still innovating. The CFPB’s own guidelines for regulatory practices emphasize this proactive approach.

The NCUA’s 2026 Supervisory Priorities: A Focus on Fair Lending and Overdrafts

In a recent letter, the NCUA Chairman highlighted three supervisory focus areas for 2026: overdraft programs, fair lending, and indirect auto lending. The emphasis on overdraft fees reflects consumer backlash over unexpected charges—something that fintech payment platforms must address promptly.

Fair‑lending reviews will scrutinize redlining, marketing, and pricing discrimination risks. Credit unions should audit their underwriting models for disparate impact and adjust pricing algorithms accordingly. In the auto lending space, NCUA is eyeing discretionary dealer mark‑ups—an area where many fintech auto lenders have found loopholes.

These priorities align closely with CFPB’s recent enforcement focus on TILA, EFTA, and ECOA, creating a regulatory environment where institutions must demonstrate robust compliance across multiple axes simultaneously.

Consumer Impact: Transparency Meets Accountability

For borrowers, the updated disclosures mean clearer pathways to dispute inaccuracies. The inclusion of accurate agency contacts ensures that consumers can reach the right authority swiftly—whether it’s filing a complaint with the CFPB or disputing a credit report error with the FDIC.

The new summary forms also give consumers an at-a-glance understanding of their rights under FCRA, empowering them to act before errors spiral into larger issues. As fintechs and traditional lenders align their disclosures with these changes, the overall transparency of consumer finance is poised to improve.

Fintech Integration: Leveraging APIs for Compliance

Many fintech firms rely on third‑party APIs to pull credit scores or generate loan estimates. The 2026 amendments require that any API response containing a credit score must also include the updated summary of consumer rights. Failure to embed this information can expose firms to legal liability.

- Action Point: Validate all API contracts against CFPB’s latest compliance checklist before deployment.

- Benefit: Ensures end‑to‑end compliance and reduces manual audit overhead.

Fintechs that have built modular compliance layers can integrate these checks seamlessly. For those still using legacy systems, a phased migration plan is essential to meet the March 20 deadline without disrupting customer experience.

Linking Finance with Innovation: The Role of Please specify the anchor text you would like translated.

Amidst this regulatory tightening, platforms that offer streamlined loan origination and underwriting—such as Please specify the anchor text you would like translated.—are positioning themselves as compliant, customer‑centric alternatives to traditional banks. By embedding real‑time compliance checks into their workflows, they can reassure both regulators and consumers that every loan meets the latest statutory requirements.

As the regulatory landscape evolves, the ability to pivot quickly will separate leaders from laggards. Firms that invest in robust compliance infrastructure now will reap long‑term benefits—reduced risk exposure, stronger customer trust, and a competitive edge in an increasingly crowded fintech market.